End of an ERA: The Bretton Woods System and Gold Standard Exchange

Fifty years ago, on August 15, 1971, then-President Nixon interrupted “Bonanza,” one of the most popular TV shows of that era. To announce that he was ending the convertibility of the U.S. dollar into gold. Many consider it to be one of the most consequential decisions (WSJ, 08/09).

President Nixon’s action of closing the gold window ended what was known as the Bretton Woods Monetary System, which had prevailed since the end of WW II.

The Bretton Woods Monetary system was the agreement of a conference from July 1 to 22, 1944 held in Bretton Woods, New Hampshire, United States.

The conference, formally known as the United Nations Monetary and Financial Conference, was a gathering of 44 nations. The conference also established the International Bank of Reconstruction and Development (now part of the World Bank) and the International Monetary Fund (IMF).

The goal of the conference was to establish cooperation among countries to avoid the problems. Such as trade wars and competitive currency devaluations, which plagued the international environment.

The Operation of the Bretton Woods Monetary System

The Bretton Woods Monetary System was not a Gold Standard, in the purest form, but it was a Gold-Exchange Standard. US political and economic dominance necessitated the dollar being at the center of the system.

After the chaos of the inter-war period, there was a desire for stability, with fixed exchange rates seen as essential for trade. But also for more flexibility than the traditional Gold Standard had provided.

The Bretton Woods system drawn up and fixed the dollar to gold at the existing parity of US$35 per ounce. While all other currencies had fixed, but adjustable, exchange rates to the dollar (World Gold Council).

What on Earth is Going on with Silver?

Watch Patrick Karim on GoldCore TV

In the case of the Bretton Woods system, only other central banks enjoyed the conversion privilege; unlike the Gold Standard, the US did not exchange gold for dollars with private parties.

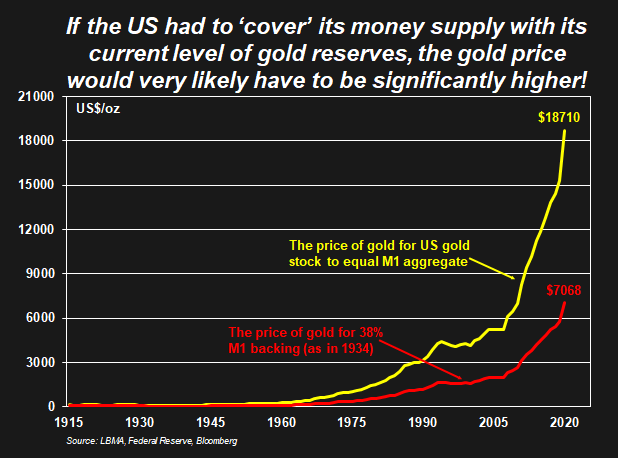

Other countries did not specifically commit to exchange their currencies for gold under Bretton Woods. There was no obligation on the US to limit its money supply to a fixed multiple of its US gold reserves.

For example, Under the Gold Standard in 1934, to cover a ratio of 38% the US M1 money supply has been limited. Or, said another way, the value of gold held in reserves had to be at least 38% of the value of the currency in circulation.

The closure of the gold window on August 15, 1971 ended this arrangement; central banks could hold US dollars as they saw fit. However, the US was no longer going to convert those dollars for gold when asked to do so.

This was not a new phenomenon under a Gold Standard as countries have always, at the end of the day, refused to exchange gold for domestic currency. When it no longer suits them to do so, be they reserve-currency countries or otherwise.

In the 1930s countries left the gold standard as they needed to deflate their currencies. When high unemployment and/or negative growth became unbearable.

And, as we saw on August 15, 1971, the reserve-currency country will also exit from a gold-exchange standard. When it refuses to honor the promise that it will convert its currency for gold with foreign central banks.

The strains of the Bretton Wood system started to show in the 1960s. Persistent, albeit low-level, global inflation made the gold price low in real terms.

The Demise of the Gold Standard

A chronic US trade deficit drained US gold reserves. But there was considerable resistance to the idea of devaluing the dollar against gold. In any event, this would have required agreement among surplus countries. To raise their exchange rates against the dollar to bring about the needed adjustment (World Gold Council).

The fundamental reason for the demise of the Gold Standard and the Gold-Exchange Standard is straightforward. Both are fixed exchange rate systems.

In the Bretton Woods System, the US dollar was fixed at $35/oz. to gold. The other currencies were fixed to the US dollar (with a band of +/-1% around the fix). To ensure the fix is maintained, But a fixed exchange rate system requires that every country applies appropriate policies to ensure the fix is maintained.

And that is the vulnerability of a fixed exchange rate system; it is inevitable that some form of economic disequilibrium will develop in the global economy; (i.e., as the result of the rise of China or the introduction of the euro).

Unpopular economic policies are required to preserve the fixed exchange rate system when disequilibrium occurs.

The signal of economic disequilibrium in a fixed exchange rate system is heavy foreign exchange market speculation against a currency.

Driving such speculation to include factors such as chronic current account deficits, declining foreign exchange reserves. Also, high rates of inflation, recessions, large budget deficits and high unemployment rates.

Whatever the specific factors, however, market speculation that the currency in question will have to be devalued (that its fix will have to be lowered) is the signal that there is disequilibrium in the system.

There was disequilibrium prior to August 15, 1971. Speculators increasingly convinced about the devaluation of the US dollar. And were accordingly going long gold, Deutschmarks, and yen.

Download Your Free Guide

The US asked Germany and Japan to raise the (fixed) value of their currencies against the dollar. Also, imposed capital controls to stop the flow of dollar investments to Europe. (The flow of dollars ended up in European central bank reserves. Under the rules of the gold exchange standard risked being converted into US gold).

Germany and Japan refused to revalue their currencies and the US refused to devalue the dollar against gold. (arguing that this the dollar/gold cross was the lynchpin of the whole system).

August 15, 1971 was the result – the US refused to exchange any more dollars for gold (it had essentially refused to do so since the late 1960s. After France converted most of its dollar holdings for gold). And the US imposed a 10% US import tariff. On all goods coming into the US (principally to induce the necessary currency revaluation abroad).

Since 1971 currencies have been floating against the dollar to a greater or lesser degree. Greater in the case of the Canadian dollar and lesser in the case of the Chinese renminbi.

Given however that dollar reserves have risen sharply since 1971, the reader can surmise. That most countries have continued the practice of deliberately keeping their currencies undervalued against the dollar.

There were various attempts in Europe to limit inter-regional currency fluctuations after August 15, 1971. These culminated with the introduction of the euro in 1999.

Is Gold Still in a Bull Market?

Watch Gareth Soloway on GoldCore TV

The euro system is a fixed exchange rate system within Europe. Indeed, the euro now too suffers from all the problems endemic to a fixed exchange rate system. (which have been solved through large loans between countries and further reaches into fiscal agreements between countries).

The Gold Standard of pre-1930s and the Gold-Exchange Standard that ended in 1971 failed to be the discipline. That governments require to do what they do not want to do. At least not when employment, welfare, and economic growth became more important policy objectives than the exchange rate.

When discipline was required (i.e. action was taken to arrest gold outflows. Including tighter monetary policies and more fiscal policy restraint. Also when these actions could then quite naturally lead to deflation, lower wages, higher unemployment, and recession) countries left the gold standard and devalued instead.

This leaves questions to ponder, such as, what role can gold serve in the international financial system? And why do central banks continue to increase their gold reserves?

From the Trading Desk

Stock Update:

Silver Britannia’s – for UK clients only. We have just taken delivery of 10,000 2021 Silver Britannia’s from The Royal Mint.

Supplies are very limited.

We are offering these at the lowest premium in the market at spot plus 44%, which includes VAT at 20%. Please contact our sales team to avail of this offer.

British Gold Sovereigns, we still have a limited number available at spot plus 5.25%. Please call our trading desk to avail of this offer.

Gold Britannia’s 1oz coins start at 6.5% over the spot.

Excellent stock and availability on all gold coins and bars with 1oz bars at a very competitive 3.75% over Spot.

Krugerrands are currently the lowest premium on 1oz coins at spot plus 5.5%.

Silver 100oz and 1000oz bars are also available VAT-free in Zurich.

Please see below our extended trading hours.

** We have extended our opening hours. Phone lines, online ordering and WebChat are now open until 09:00-22:00 (Europe/Dublin) USA 09:00 to 17:00 EST**

Market Update:

Friday we got the US nonfarm payroll data for July and it came in stronger than expected at 943,000, the forecast had been 880,000.

Gold and Silver sold off as it’s seen that it may speed up plans for the Federal Reserve to withdraw support ‘tapering’ from the economy.

What followed on from there however was unusual to say the least.

When the Asian markets opened large sell orders were placed in a very illiquid market which resulted in Gold falling 4% just after the open and Silver close to 7% with prices recovering shortly after in the Asian morning session.

The question everyone is asking, what caused such a big gap down and possible reasons behind it.

From the information that is out there at the moment, let’s look at some of the possible causes:

1. A fund selling a large holding – This would seem highly unlikely that a fund would sell such an amount into an illiquid market unless a forced sale due to something like a margin call or liquidity event.

2. A fat-fingered trade – Possible but again very unlikely.

3. A large player establishing a new or adding to an existing position – Similar to #1, it would not make sense to add to a current or new position of this size into a un liquid market

4. Unilateral selling by a Central Bank or Bullion Banks

5. Co-ordinated selling by Central Banks and Bullion Banks

Both #4 & 5 above are plausible as they would have the greatest effect when executed in an illiquid markets but that leads to why? We don’t know the answer yet and we may not get one.

One big change happening in the Gold market is Basel 111 and how Gold is classified as an asset.

We covered Basel 111 in an earlier market update in July this year and it is worth a read if you missed it.

How Will Basel III Impact the Gold Market? – GoldCore Gold Bullion Dealer

From a fundamentals perspective, the whole move was not justified. There was no other sell-off in other markets, there was no new news events.

From a price perspective, the RSI is oversold and is due to bounce. We have moved higher, looking to consolidate and hold onto these gains.

Buy Gold Coins

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

10-08-2021 1729.55 1723.35 1248.22 1244.60 1475.13 1471.05

09-08-2021 1741.50 1738.85 1253.88 1254.06 1481.32 1479.24

06-08-2021 1799.45 1762.90 1292.90 1269.64 1523.59 1497.58

05-08-2021 1811.20 1800.75 1302.07 1294.92 1529.74 1521.63

04-08-2021 1812.45 1829.10 1301.34 1311.83 1528.44 1538.82

03-08-2021 1809.70 1812.65 1300.81 1305.11 1523.04 1527.16

02-08-2021 1807.55 1811.45 1298.36 1302.61 1521.05 1524.34

30-07-2021 1828.25 1825.75 1307.75 1308.52 1535.73 1536.92

29-07-2021 1819.45 1829.30 1304.00 1309.05 1532.16 1539.54

28-07-2021 1799.30 1796.60 1296.04 1297.15 1522.03 1524.24

Buy gold coins and bars and store them in the safest vaults in Switzerland, London or Singapore with GoldCore.

Learn why Switzerland remains a safe-haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here